Low Consumer Demand Is An Opportunity To Rebuild

The pandemic led to a surge in consumer goods demand as the world gradually emerged from lockdowns. The UK alone had an impressive 18% growth rate.

Since then, things have slowed down. The so-called ‘Bullwhip Effect’ caused excess inventory across the USA, Europe and Europe, and consumers felt the impact of geopolitical instability, high interest rates and other factors. We have been in a kind of recession for some time, even if the official data doesn't say so.

Consumer Demand Trends from 2019 through to 2024 in the UK and USA

United Kingdom:

2019: Pre-pandemic levels of consumer spending were considered the baseline.

2020: The onset of the COVID-19 pandemic saw a significant decline in consumer spending due to lockdowns and restrictions.

2021: A recovery phase began, with spending increasing by 17.89% from 2020.

2022: Growth continued, albeit at a slower pace.

2023: A slight decrease in Q4 compared to Q3, with a negative 0.1% growth rate.

2024: The latest data suggests a cautious consumer sentiment, with trends indicating a focus on essential spending and value-seeking behavior.

United States:

2019: Established as the last normal year for consumer spending before the pandemic.

2020: Experienced a sharp decline in consumer spending, particularly in services like travel and dining.

2021: Saw a rebound in spending as restrictions eased and vaccination rates increased.

2022: Continued recovery with increased spending in various sectors.

2023: Data indicates a stabilization of consumer spending with a shift towards services over goods.

2024: Early indicators point to a steady but cautious spending pattern, with consumers being mindful of economic uncertainties.

The trend from 2019 to 2024 shows a rapid decline due to the pandemic, followed by a period of recovery and stabilization. The year 2024 seems to be a year of cautious optimism, with consumers prioritizing essential purchases while being aware of economic conditions.

Now is the ideal time to rebuild supply chains while the demand continues to stabilize. The lower demand will mean lower risks and the opportunity to source from manufacturers closer to your consumer markets. There are many ways to do this and participate in the trends towards reshoring and nearshoring. Avoiding the challenges in the Red Sea and the increasing geopolitical tensions is forcing supply lines to be completely reconfigured.

We have been helping clients with where these sources are best located. Distributing across several options is a smart move and does require some effort in moving away from the dominance of China in the manufacturing space. However, the firms that are doing this are already seeing strong progress in new production from Latin America, Mediterranean and manufacturing challenger nations in Asia. For example, Vietnam exceeded its own government's target in 2022 with 8.02% growth recorded and continues to grow beyond expectations.

What happens when demand increases and when will this be?

The Bank of England’s Monetary Policy Report recently indicated that demand growth is expected to remain weaker than potential supply growth from 2024 through to 2027. And in the USA, the Congressional Budget Office’s outlook suggests that stronger-than-expected economic growth as recent as 2023 could affect rates and economic activity through to 2027. Consumer patterns are also changing with multiple reports of consumer behavior defying expectations with changing habits.

These reports suggest that while there may be growth in consumer demand, it is not expected to rise sharply by 2027. Instead, growth seems to be more moderate and dependent on various economic and social factors.

The message here is clear. There is a period of quieter economic activity that will last for three years which is the best time to re-design supply chains.

And when the demand does increase, it will be in a very different set of trade flows than those we saw before 2019. Just this morning (12th June 2024) in a discussion with Michael Boulton we discussed the growing demand from the UK to USA and Australia which continues to be strong despite the economic headwinds elsewhere. And in that mix we now see Japan with a healthy appetite for consumer technology exported from the UK and USA. These are more than a few green shoots and align with the political bonding that has been strengthening between these nations.

Summary

We can see how consumer spending trends from 2019 to 2024 have created opportunities for companies to re-design their supply chains. By reshoring or nearshoring their production, companies can diversify their sources, avoid geopolitical risks, and tap into new markets. Some countries, such as Vietnam, Japan, and the UK, are emerging as strong partners in this new landscape.

Do you want to transform your supply chain and gain a competitive edge in the global market? Visit our website at www.BostonWarwick.com and learn how we can help you. We are a leading consultancy firm with expertise in supply chain, aviation, and international trade. We help companies unlock value creation by re-engineering their end-to-end supply chains.

References

https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/state-of-consumerhttps://www.ons.gov.uk/economy/nationalaccounts/satelliteaccounts/datasets/consumertrends/currenthttps://www.bankofengland.co.uk/-/media/boe/files/monetary-policy-report/2024/may/monetary-policy-report-may-2024.pdfhttps://www.pwc.com/gx/en/industries/tmt/media/outlook/insights-and-perspectives.htmlhttps://www.cbo.gov/publication/59946https://www.ons.gov.uk/economy/nationalaccounts/satelliteaccounts/bulletins/consumertrends/octobertodecember2023https://www.ons.gov.uk/economy/nationalaccounts/satelliteaccounts/timeseries/abjr/pn2

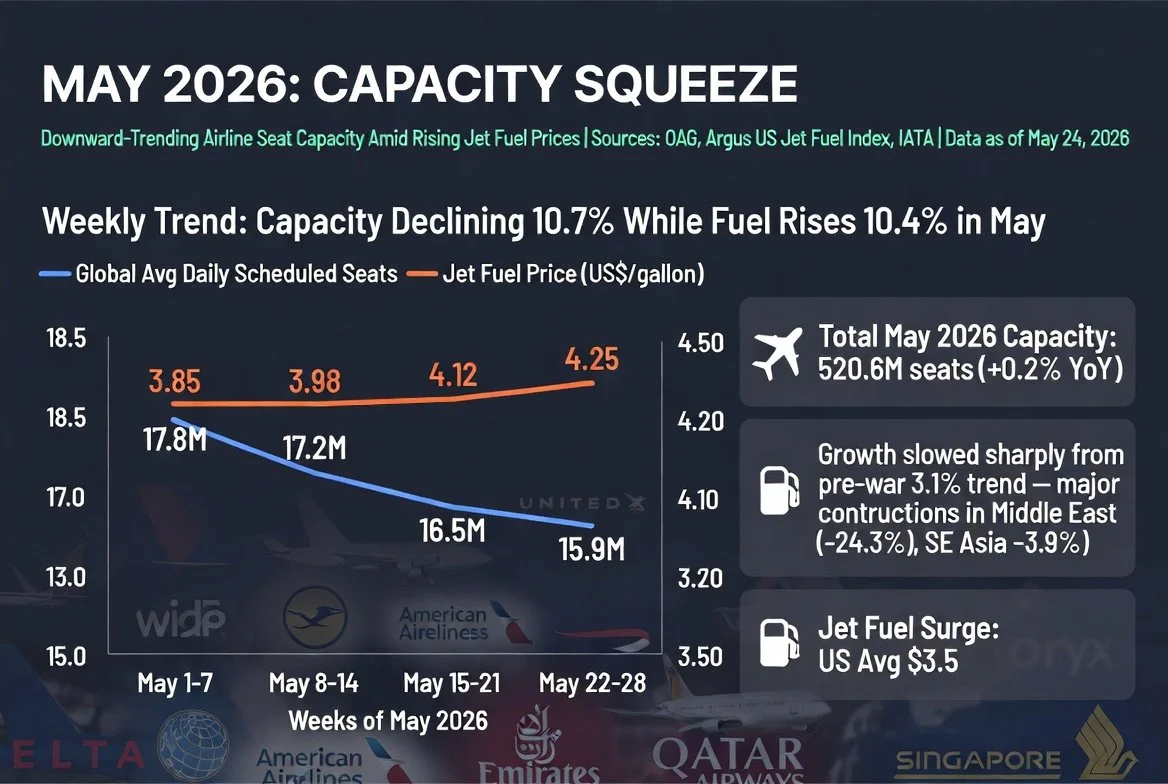

Europe’s jet-fuel stocks continue to fall as the Hormuz crisis enters its fourth month. Our latest Top 50 ranking shows Budapest and Warsaw entering the list while UK airports push back against proposed EU261 relief for airlines.