Aviation Executive Briefing May 18-24 2026: American’s 4 Europe Routes, FAA $1B & Fuel Risk Deep Dive

Boston Warwick drives transformative change for airlines, airports, and aviation stakeholders. Its expert team, with decades of experience, delivers high-impact projects in flight operations, fleet valuations, and M&A, empowering clients with strategic insights.

This week’s report unpacks critical developments from May 18 to May 24, 2026, highlighting new transatlantic route launches, FAA infrastructure investments, ongoing capacity adjustments amid fuel pressures, and key airport modernization projects amid record summer demand forecasts.

Airlines

American Airlines Launches Four New Nonstop European Routes

Image: American Airlines Boeing 787-8 Dreamliner on transatlantic service | American Airlines

American Airlines executed one of the most ambitious single-week European network expansions in its recent history on May 21, 2026, launching four new seasonal nonstop routes that materially strengthen its position in Central and Southern Europe. The carrier introduced daily and near-daily service from Philadelphia (PHL) to Budapest (BUD) and Prague (PRG), alongside Dallas-Fort Worth (DFW) to Athens (ATH) and Zurich (ZRH). All four routes are operated exclusively with Boeing 787-8 Dreamliners in a three-class configuration featuring 34 lie-flat business class suites with direct aisle access, 24 premium economy seats, and 182 economy seats with enhanced legroom and in-seat power. This marks American’s first scheduled service to Budapest and Prague, two markets that have seen passenger demand grow 28% since 2023 according to IATA data, driven by cultural tourism, business travel to the EU’s eastern flank, and strong VFR flows from the large Hungarian and Czech diaspora communities in the Northeast and Midwest United States.

Strategically, these additions diversify American’s European portfolio away from the heavily contested London, Paris, and Madrid corridors where yields have softened 6-9% year-over-year. Budapest and Prague offer lower slot costs and less congestion than Western European majors, while Athens provides critical summer leisure feed into the carrier’s codeshare partners Aegean Airlines and Volotea. Zurich serves as a high-yield business gateway to German-speaking Europe and strengthens American’s competitive stance against United’s Newark-Zurich service. Early booking data released internally shows load factors already averaging 64% for the first 90 days of operation, with premium cabin advance purchase rates 11% above system average. For revenue management teams, the routes represent a textbook application of “right-gauge” long-haul deployment: the 787-8’s 7,000+ nautical mile range and 15% better fuel burn versus legacy 767s allow profitable operation even at moderate load factors. Network planners should note that these services also create new one-stop opportunities from American’s Caribbean and Latin American hubs into Eastern Europe, potentially cannibalizing some existing codeshare volumes but expanding total addressable market. Executives evaluating competitive response should anticipate Delta and United to file similar applications for 2027 summer authority on overlapping city-pairs.

Alaska Airlines and Delta Add Seattle-Europe Capacity

Image: Alaska Airlines and Delta Air Lines long-haul expansion from Seattle | Alaska Airlines / Delta Air Lines

The Pacific Northwest emerged as the most competitive long-haul battleground this week as Alaska Airlines and Delta Air Lines simultaneously announced major capacity additions from Seattle-Tacoma International Airport (SEA). Alaska launched daily Seattle-London Heathrow service utilizing its 787-9 Dreamliners equipped with 34 fully enclosed lie-flat suites, premium economy, and a spacious 174-seat economy cabin optimized for the 4,800-mile sector. The carrier also added seasonal daily flights to Reykjavik Keflavik starting May 28, capitalizing on Iceland’s popularity as a summer gateway to Europe for West Coast travelers. In a direct countermove, Delta introduced 4x-weekly Seattle-Rome Fiumicino and 3x-weekly Seattle-Barcelona rotations operated by Airbus A330-900neos, expanding its Seattle transatlantic footprint to five destinations and creating the only U.S. carrier service to both Rome and Barcelona from the Pacific Northwest.

This escalation reflects structural demand growth: Cirium schedule data shows SEA-Europe passenger volumes surged 19% year-over-year in Q1 2026, outpacing the national average of 11%. Alaska’s strategy leverages its 787-9’s superior fuel efficiency (approximately 18% better than older 767-300ERs still flown by some competitors) and strong brand loyalty among Pacific Northwest leisure travelers. The Reykjavik service, in particular, offers attractive fifth-freedom opportunities and positions Alaska as the preferred carrier for multi-destination European itineraries. Delta’s A330neo deployment prioritizes cargo belly capacity on leisure-heavy routes, with each aircraft offering 15-18 tons of freight payload that can generate $180,000-$220,000 in ancillary revenue per round-trip during peak summer. For both carriers, early yield indications are encouraging: premium cabin fares on the new LHR and FCO services are averaging 9% above 2025 levels for comparable sectors. Executives at other U.S. carriers should view this as a signal that secondary European gateways from non-traditional hubs can be sustainably served with modern widebodies, potentially influencing future fleet allocation decisions for the 2027-2028 seasons. The Seattle-Europe corridor is now one of the fastest-growing long-haul markets in North America and warrants close monitoring for slot and gate constraints at SEA’s international terminal.

United Airlines Deploys 737 MAX 8 on Newark-Santiago de Compostela Route

United Airlines made aviation history on May 22, 2026, by inaugurating the first regularly scheduled nonstop service from the United States to Santiago de Compostela (SCQ), Spain, with thrice-weekly seasonal flights from Newark Liberty International Airport (EWR). The route is operated with Boeing 737 MAX 8 aircraft in a two-class configuration featuring 16 premium seats and 144 economy seats, providing a more intimate long-haul experience than widebody competitors on the Iberian Peninsula. Santiago de Compostela, the capital of Galicia and endpoint of the world-famous Camino de Santiago pilgrimage route, attracts over 400,000 international visitors annually, with strong growth from North American faith-based and cultural tourists since UNESCO recognition and improved marketing by the Spanish tourism board.

This deployment exemplifies United’s ongoing “right-size” philosophy for secondary European markets where widebody economics are marginal outside peak summer. The 737 MAX 8’s 3,500-nautical-mile range comfortably covers the 3,200-mile EWR-SCQ sector with favorable winds, while its 14% lower fuel burn versus the 737-900ER allows profitable operation at load factors as low as 72%. Initial booking curves show 78% load factor projections for the June-September window, with premium cabin advance purchases running 14% above system average for similar narrowbody long-haul routes. The service also creates valuable connections for United’s East Coast and Midwest hubs into a region previously requiring connections through Madrid or Lisbon. For revenue management, the route provides real-world data on price elasticity in emerging pilgrimage and culinary tourism markets; average round-trip fares of $1,049 suggest healthy margins despite the smaller aircraft. Network planners should treat this as a replicable template for future point-to-point services to secondary European cities such as Porto, Bilbao, or Valencia in the 2027 summer season, particularly as the MAX 10 enters service and offers even greater range and capacity flexibility.

Qatar Airways Expands African Footprint with Port Sudan Service

Qatar Airways announced three weekly flights to Port Sudan International Airport (PZU) effective late May 2026, significantly enhancing connectivity to Sudan and the broader Horn of Africa region. Operated with Airbus A320 family aircraft configured in two-class layout, the service positions Doha (DOH) as the premier gateway for business, humanitarian, and diaspora traffic into a market that has seen limited scheduled international airline presence since regional instability began to ease. This expansion continues Qatar’s aggressive African growth trajectory, which now encompasses 12 destinations across the continent and leverages the carrier’s extensive fifth-freedom rights and codeshare partnerships with African majors.

For cargo executives, the route offers immediate value through belly capacity for high-value Sudanese exports including gum arabic, sesame, and livestock products, with projected annual freight revenue exceeding $12 million in the first year. Passenger demand is driven by a combination of Sudanese diaspora returning for summer, NGO and UN personnel movements, and growing business interest in Sudan’s agricultural and mining sectors. Yield management will be critical given the thin route economics and competitive overlap with Ethiopian Airlines and EgyptAir on regional flows; however, Qatar’s superior product and on-time performance record provide a meaningful differentiator. Industry observers interpret this move as part of a broader strategic shift by Gulf carriers to fill gaps left by European majors retreating from secondary African markets amid high fuel costs and pilot shortages. Executives at competing carriers should monitor load factor and yield performance closely, as successful stabilization of this route could accelerate similar expansions by Qatar and Emirates into other under-served Horn of Africa and Sahel markets in 2027.

Mergers, Acquisitions & Finance

Ongoing Consolidation Discussions in U.S. Legacy Sector

Industry sources confirmed this week that senior executives at multiple U.S. legacy carriers have engaged in exploratory discussions regarding potential combinations, testing the boundaries of the current administration’s antitrust enforcement posture. While no formal merger applications or joint venture filings have been submitted, conversations have reportedly included high-level briefings to Department of Justice and Department of Transportation officials on the strategic rationale for further scale in a domestic market where the four largest carriers already control approximately 75% of seat capacity. The timing is notable: sustained cost inflation, new pilot contract economics averaging 30-40% pay increases since 2023, and the imperative for greater international network density to compete with foreign mega-carriers have created renewed interest in consolidation among boards and investors.

For M&A and corporate strategy teams, the critical variable is deal structure. A full statutory merger would face intense scrutiny on overlapping domestic routes and slot holdings at constrained New York and Washington airports, likely requiring divestitures similar to those imposed on the Alaska-Hawaiian transaction. A more limited equity tie-up or expanded joint venture on international routes might navigate review more easily while delivering meaningful cost synergies through shared procurement, maintenance, and technology platforms. Historical precedent suggests that deals framed around clear consumer benefits—new routes, enhanced loyalty program reciprocity, and schedule improvements—have higher clearance probability. Executives should model multiple scenarios, including the impact of any remedy packages on hub economics and the potential for foreign carrier alliances to gain relative advantage if U.S. consolidation stalls. The political window for such discussions may narrow materially ahead of the 2028 election cycle, making 2026-2027 the most plausible period for any formal moves.

Leasing Sector M&A Activity Continues

Aircraft leasing platform consolidation remained a defining theme this week, with continued momentum toward larger, better-capitalized entities following several high-profile transactions in late 2025 and early 2026. The drivers are structural: lessors require greater scale to diversify across aircraft types, geographies, and lessee credit profiles; access to public debt and equity markets improves with size; and airlines increasingly demand comprehensive fleet solutions that include sale-leaseback packages, end-of-life remarketing, and flexible lease terms for next-generation narrowbodies. Recent activity has included acquisitions of regional lessors and portfolios by larger platforms, further reinforcing Ireland’s status as the global center of gravity for aircraft leasing.

For airline CFOs and fleet acquisition teams, this consolidation has direct implications. Fewer but stronger lessors mean greater negotiating leverage for carriers with investment-grade credit ratings, particularly on high-demand assets such as the 737 MAX 10 and A321XLR. Financing costs for new deliveries remain elevated through at least 2027, with all-in lease rates for new narrowbodies 12-18% above 2023 levels. Carriers should therefore prioritize multi-year sale-leaseback commitments with the largest platforms to lock in capacity and pricing. Watch for additional announcements in the second half of 2026 as private equity dry powder continues to seek deployment in aviation assets with predictable cash flows and strong residual value characteristics.

Airport Developments

FAA Announces Nearly $1 Billion for Family-Friendly Airport Enhancements

Image: U.S. airport family amenities modernization | Federal Aviation Administration

On May 18, 2026, U.S. Transportation Secretary Sean P. Duffy announced nearly $1 billion in new federal funding to modernize airports nationwide with enhanced family-oriented amenities and accessibility improvements. The investment, drawn primarily from the Infrastructure Investment and Jobs Act and the Airport Improvement Program, targets both large-hub and smaller regional facilities to address passenger experience gaps that have become increasingly visible as domestic and international travel volumes return to and exceed pre-pandemic peaks. Specific allocations include expanded children’s play zones with age-appropriate equipment, dedicated nursing and lactation rooms with privacy and power infrastructure, improved family wayfinding and stroller-friendly security lanes, and enhanced facilities for passengers with disabilities and limited mobility.

The initiative also includes a separate $26 million tranche for pilot and maintenance technician workforce development programs, recognizing that staffing shortages remain the single largest constraint on capacity growth at many carriers. A companion FAA program to standardize controller training curricula and accelerate recruitment pipelines was unveiled the same day, with the goal of reducing average training timelines from 3-5 years to a more predictable 2.5-3 year cycle while maintaining the highest safety standards. For airport executives and commercial teams, these investments represent a rare opportunity to accelerate capital projects that have been shown in pilot programs to increase non-aeronautical revenue by 15-22% through longer dwell times and higher passenger satisfaction scores. Family-focused amenities in particular have become a key differentiator in airline and airport choice, especially for the growing segment of multi-generational leisure travelers. Executives should prioritize projects that can be completed within 18-24 months to capture the full summer 2027 and 2028 travel seasons.

Houston Hobby Airport Advances Major Terminal Expansion

Image: Houston Hobby Airport third concourse and international hub rendering | Houston Airports

Houston Hobby Airport (HOU) continued visible construction progress this week on its $344 million expansion program, with steel erection advancing on the new third concourse, six additional gates, expanded Club and premium passenger spaces, taxiway extensions, and a significantly enlarged concessions program. The project, which broke ground in late 2024, is on schedule for substantial completion in 2027 and will increase the airport’s gate capacity by approximately 25%, providing critical relief for Southwest Airlines’ growing Houston operation and enabling new international services. Design features include solar-ready roofing, electric ground support equipment charging infrastructure, and advanced baggage handling systems designed to reduce mishandling rates below the industry average of 2.5 bags per 1,000 passengers.

For airlines operating at HOU, the expansion addresses long-standing gate and hold-room constraints that have limited schedule flexibility during peak summer and holiday periods. The new concourse will feature 40% larger hold rooms, dedicated family security lanes, and improved connectivity to the existing terminals, directly responding to passenger feedback on congestion. Airport leadership has already initiated discussions with additional carriers regarding new routes once the facility opens; early interest has been expressed in Caribbean leisure destinations, Mexican resort gateways, and potentially one or two Central American business routes. Executives at Southwest and other HOU operators should incorporate the 2027 capacity increase into their network and fleet planning models for the Texas market, where enplanement growth has averaged 7% annually since 2023 and shows no signs of slowing. The project also positions Hobby as a more credible competitor to George Bush Intercontinental (IAH) for certain international flows, potentially shifting some connecting traffic patterns within the Houston metroplex.

Ongoing Expansions at Major U.S. Hubs

The largest airport capital investment cycle in U.S. history continued to advance across multiple major gateways this week. At New York JFK, the $9.5 billion New Terminal 1 project—part of the broader $19 billion public-private redevelopment—reached key structural milestones, with the first phase of the 1.2 million square foot facility now on track for partial passenger operations in late 2026. The terminal will ultimately feature 23 gates, a 1,000-foot-long headhouse, and direct connections to the AirTrain and subway systems. Dallas-Fort Worth’s $12 billion DFW Forward program saw continued progress on Terminal C modernization and detailed planning for the entirely new Terminal F, which will add 15-18 gates optimized for narrowbody and regional operations. Los Angeles International Airport’s $30+ billion landside access modernization program advanced on the automated people mover, consolidated rental car center, and multiple terminal upgrades in preparation for the 2028 Olympic and Paralympic Games.

These concurrent projects represent a once-in-a-generation reshaping of U.S. hub infrastructure and will have profound implications for airline network strategy, slot allocation, and competitive positioning over the next 15-20 years. Airlines with significant operations at these airports should engage immediately on gate and facility allocation negotiations, as legacy space assignments are being fundamentally revisited in light of new capacity and passenger flow designs. The scale of investment also signals strong long-term confidence in U.S. aviation demand; FAA long-term forecasts project 1.3 billion enplanements by 2035, with international traffic growing at 4.2% CAGR. Executives evaluating hub strategies for the next decade must incorporate these infrastructure timelines into their 5-, 10-, and 15-year fleet, network, and capital plans, particularly as new entrants and foreign carriers seek access to the enhanced facilities.

Industry Innovations & Services

FAA Advances Controller Pipeline and Training Standardization

The FAA unveiled a comprehensive new workforce development program on May 18 aimed at strengthening the air traffic controller pipeline through standardized training curricula, accelerated recruitment pathways, and expanded simulation-based instruction. The initiative directly addresses persistent staffing shortfalls that have contributed to ground delay programs, capacity constraints, and passenger frustration at several major terminal radar approach control and enroute facilities. By standardizing core competency requirements across facilities and leveraging advanced simulation technologies, the agency expects to reduce average training time from the current 3-5 years to a more predictable 2.5-3 year timeline while preserving the uncompromising safety standards that have made the U.S. National Airspace System the safest in the world.

For airline operations, dispatch, and network planning executives, this development offers measured optimism for improved airspace and airport throughput efficiency by 2028-2029, particularly on high-density corridors such as the Northeast megalopolis, Florida, and transcontinental routes. However, near-term relief will be limited; the current controller shortage, estimated at 3,000-4,000 positions system-wide, will continue to constrain schedule reliability through at least summer 2027. Carriers should therefore maintain conservative block time padding, continue aggressive participation in Collaborative Decision Making (CDM) and surface management initiatives, and factor potential delay propagation into their irregular operations contingency planning. The long-term payoff, if the program meets its targets, could be material: even a 10% reduction in average delay minutes per flight would generate hundreds of millions of dollars in annual cost avoidance across the industry.

Airlines Prepare for Record Spring/Summer Passenger Volumes

U.S. airlines entered the Memorial Day weekend with forecasts for another record-breaking travel period, with Airlines for America projecting 171 million passengers for the March-April spring shoulder alone—a 4% increase over the comparable 2025 period. Daily volumes are expected to average 2.8 million passengers system-wide, supported by a modest 2% increase in flights and available seats as carriers add capacity strategically on leisure-heavy routes while exercising continued discipline on marginal domestic segments amid elevated fuel costs and pilot contract economics. Global capacity data compiled by Cirium for May 2026 presents a more nuanced picture, with schedules trimmed by approximately 3% compared to the prior year—equivalent to roughly 13,000 cancelled flights and 2 million seats removed across the world’s 20 largest carriers. Nineteen of those 20 carriers implemented some form of schedule reduction, reflecting a combination of fuel price volatility, supply chain constraints on aircraft availability, and a deliberate shift toward margin protection over market share gains.

The net result is a more balanced supply environment that should support stable or modestly improving unit revenues through the peak summer season, provided fuel prices do not spike further. Premium cabin demand remains the standout performer, with many carriers reporting business class load factors above 90% on key long-haul routes and premium economy continuing to outperform expectations. For revenue management and network teams, the lesson is clear: capacity discipline, dynamic pricing, and aggressive ancillary revenue strategies will be essential to translate record passenger volumes into record profits. Executives should also prepare for continued volatility; any escalation in geopolitical tensions or jet fuel supply disruptions could trigger rapid schedule adjustments and surcharge implementations. The summer of 2026 is shaping up to be a test of operational resilience and commercial agility rather than pure growth.

Key Watch Items

Capacity Adjustments and Fuel Market Volatility

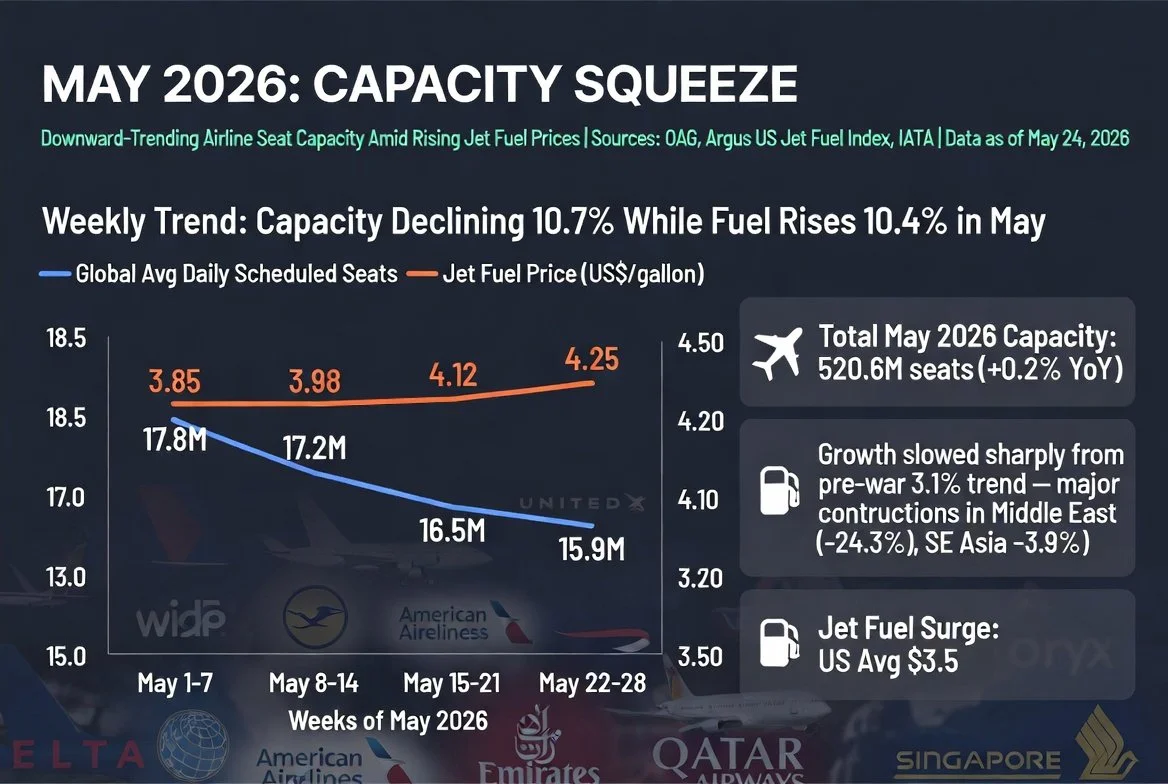

Image: Global airline capacity adjustments and jet fuel price volatility May 2026 — For deeper weekly updates on the 47 airports and 12 countries most at risk of fuel supply disruptions this summer, visit our dedicated series at BostonWarwick.com/blog

The global aviation sector entered the final week of May with accumulating signals of capacity discipline that are beginning to meaningfully reshape summer 2026 outlooks and pricing power. Cirium’s latest schedule analysis indicates that reductions have been most pronounced among European and Asian carriers facing both elevated fuel costs and softening yields on certain long-haul leisure markets, while U.S. domestic capacity growth has been held to low single digits despite robust underlying demand. The net effect is a more balanced supply environment that should support stable or improving unit revenues through the peak season, provided macroeconomic conditions and fuel markets remain within current ranges. Nineteen of the world’s twenty largest airlines have made some form of schedule adjustment this month, with the aggregate impact equivalent to approximately 13,000 cancelled flights and 2 million seats removed from the global market.

For fuel and treasury teams, volatility remains the dominant near-term risk. Jet fuel crack spreads have widened noticeably in recent weeks, and any escalation in geopolitical tensions—particularly in the Middle East or around key refining hubs—could trigger rapid price spikes. Airlines with active hedging programs covering 40-60% of 2026 requirements are materially better positioned; those with lower coverage may face meaningful margin compression if prices move sustainably above $3.00 per gallon. Executives should review fuel surcharge mechanisms, ancillary revenue optimization, and dynamic pricing algorithms to maintain profitability under various fuel price scenarios. This week’s capacity adjustments also underscore a broader strategic shift: carriers are increasingly willing to sacrifice marginal volume in order to protect yields and unit revenues, a discipline that was notably absent in the immediate post-pandemic recovery phase.

For much deeper analysis—including our proprietary weekly updates tracking the 47 airports and 12 countries currently assessed as most at risk of fuel supply disruptions through the 2026 summer peak—readers are encouraged to visit the dedicated Fuel Risk Tracker series on our website at www.BostonWarwick.com/blog. These posts provide granular route-level exposure data, hedging strategy benchmarks, and scenario modeling that go well beyond the high-level summary presented here.

Safety and Regulatory Developments

Minor incidents involving older turboprop aircraft, including two Antonov An-2 accidents in remote regions of Central Asia and Russia, served as timely reminders of the continued importance of rigorous maintenance oversight and airworthiness directive compliance for regional and general aviation fleets. While these events did not involve commercial passenger operations, they highlight the diverse risk profile across the global fleet and the need for operators of legacy equipment to maintain heightened vigilance. On the regulatory front, the FAA’s May 18 workforce and infrastructure announcements signal a proactive, investment-oriented approach to capacity constraints, but the agency continues to face external scrutiny over certification timelines for new aircraft variants, engine modifications, and advanced air mobility concepts.

Safety management system (SMS) implementation deadlines for Part 121 carriers remain on track, with several major airlines reporting successful integration of predictive analytics and machine-learning models into their risk assessment and safety assurance processes. Executives should ensure that SMS data feeds are fully aligned with flight operations, maintenance, and dispatch systems to capture leading indicators of potential issues before they manifest in operational disruptions or incidents. The overall regulatory environment is expected to remain stable and predictable through the balance of 2026, providing a constructive backdrop for long-term fleet, network, and capital planning. Carriers that treat safety and compliance as strategic enablers rather than cost centers will be best positioned to navigate any future policy shifts.

Get Weekly Executive Insights

Join 12,000+ aviation leaders receiving Boston Warwick’s unfiltered briefings every Sunday morning.

Subscribe Free →